Product People Drove Efficiency and Growth by Unlocking Lending Scalability and User Growth With Seamless Product Leadership

About how we redesigned and automated the account closure journey, reducing manual workload and minimizing reliance on collection agencies, reducing losses ~€244K

The Client: European Union Unicorn Banking

The client that we worked with is a leading digital bank based in Berlin, Germany, renowned for its rapid growth and innovative approach to banking. Founded in 2013, it quickly disrupted the traditional banking sector with its user-friendly mobile banking solutions.

The company experienced exponential growth, amassing over 7 million customers across 25 markets by 2023. Key to its success was securing substantial investments, including a $300 million Series D funding round in 2019 and an additional $470 million in Series E in 2021, boosting its valuation to $9 billion.

The Mission: Interim Product Manager

With key deadlines approaching and bold growth targets on the horizon, European Union Unicorn Bank was facing a critical gap. The Lending team - responsible for some of the most strategically important product work - was suddenly lacking full-time product leadership, one PM leaving, and the Lead PM moving to part-time. What followed was a natural slowdown: decisions stalled, clarity faded, and momentum across critical initiatives was being lost.

Product People stepped in with one mission: to provide immediate structure, leadership, and continuity - not just maintaining operations, but to help the company push forward with confidence. We organized a rapid kickoff, clarified short-term goals, and created visible early wins to rebuild team confidence and momentum

Our mission focused on two initiatives vital to both business growth and operational resilience. First, we set out to streamline the integration with credit bureaus - a foundational step to unlock rapid, scalable lending expansion across new European markets. The main bottlenecks were inconsistent data formats across different bureaus, significant time spent internally correcting those errors, and reporting challenges due to each bureau requiring different report structures. By addressing these issues, we aimed not only to speed up market entry but also to lay the groundwork for sustainable, long-term growth. At the same time, we redesigned the account closure journey for lending users to eliminate compliance risks and operational roadblocks. This work addressed both regulatory demands and user experience pain points, ensuring that every customer offboarding was secure, efficient, and transparent. Together, these efforts positioned the business to grow with agility while staying ahead of industry standards.

Once the Lending team was stabilised and new hires had ramped up after our handover, we pivoted to the Savings product. The Savings team was left without product leadership, with the Savings Product Manager going on parental leave. Having already proven our ability to adapt and deliver, we were asked to shift seamlessly into this new domain.

Our ability to quickly adapt to new domains and teams ensured continuity and progress across both Lending and Savings. Across two distinct product areas (and two entirely different teams), we brought speed, clarity, and consistency when it was needed most. And most importantly: we kept things moving forward.

Our Main Quest: Driving faster Lending Expansion through Credit Bureau Integration

🌐 Simplifying Credit Bureau integration: From manual to automated

European Union Unicorn Bank faced a critical challenge:

Launching lending products in a new country requires integrating individually with each local credit bureau.

This was a slow and complex process with major pain points:

- Each credit bureau used different data formats (e.g., dates, identifiers, income categories), leading to manual errors and more support tickets

- Each integration required a lengthy internal third-party assessment, adding time and complexity to the process

- Significant engineering effort was required for each integration - both in discovery and delivery - further limiting how quickly the bank could scale

- Each bureau asked for different reports (what data to send, how often, in what structure), requiring manual adjustments by teams to adapt to each bureau’s requirements, and making expansion into new markets slow and resource-intensive

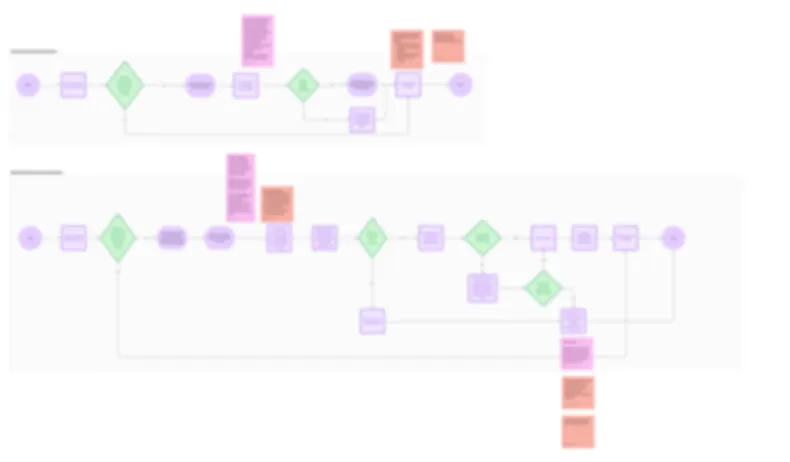

Our Role: Onboarding an External Partner to Simplify and Scale

A key challenge was connecting a third-party integration platform with the bank’s internal systems - matching its capabilities to the bank’s needs ****with the realities of the engineering and product teams, and ensuring it could truly support scalable growth across markets.

Product People stepped in to:

- Scope the exact product requirements for the bank’s use case: We ran focused discovery sessions with Engineering, Legal, and Product teams to understand internal constraints and align expectations with the vendor’s capabilities. This helped define a clear, realistic scope tailored to the bank’s actual needs.

- Align Legal, Engineering, and external teams to ensure smooth collaboration: We mapped responsibilities and set up clear communication flows across engineering, compliance, legal, and the external provider - reducing ambiguity and enabling smoother collaboration throughout the project.

- Support technical discovery, clearing the way for implementation: the process **included checkpoints to assess risks and align all relevant departments (Risk, Legal, Data Protection, etc.) before launch. We ensured all dependencies were managed and teams aligned, helping the project move forward without blockers.

The Impact

This integration will significantly reduce bureaucracy by having the external partner:

- Normalize and format data points automatically, eliminating manual fixes

- Handle all credit bureau communications, ensuring each one gets the correct data and reports

- Make expansion into new markets far faster, meeting business goals

By leading the onboarding and scoping process, Product People set the foundation for scalable Lending growth across Europe.

Initiative 1 - Compliant Account Closure for Lending Customers

Problem:

When customers with active loans initiated account closure, the process at European Union Unicorn Bank wasn’t fully compliant. Without proper consent flows and automated checks, remaining loan repayments couldn’t always be recovered directly from the user’s personal account. This led to:

- €244K in financial losses in 2024, due to refunded balances on accounts with unresolved debts

- A 28% potential recovery gap, based on funds that could have been collected before closure

- A growing number of manual escalations and support tickets, involving BankingOps, Tech, and Collections teams

- Legal obligations to close accounts within 2–3 working days, even if outstanding loans were not yet resolved

What has been done:

- Mapped the full user journey for customers with Consumer Credit and Transaction-Based Installment Loans.

- Redesigned the off-boarding flow to ensure required consents and automated checks are completed before closure

- Implemented end-to-end automation, removing manual blockers and reducing operational dependency

- Partnered closely with Risk, Legal, Compliance, and Ops teams to guarantee alignment and secure sign-off

Outcome:

The new journey provided a fully compliant and streamlined process, significantly reducing manual work for internal teams and improving the customer experience. This change also set a scalable foundation for future offboarding processes.

Initiative 2 - Strategic Deposit Allocation to a Partner Financial Institution

Problem:

To ensure long-term financial stability, European Union Unicorn Bank needed to enhance how it managed liquidity through a more strategic deposit allocation approach. The goal was to distribute a portion of customer deposits to a partner financial institution - in a way that ensured regulatory compliance, minimized financial risk, and didn’t block key product or market initiatives. Achieving this required tight coordination between multiple internal teams and external stakeholders.

What has been done:

- Aligned cross-functional teams across risk, legal, operations, and engineering to define clear ownership and next steps

- Coordinated with the external financial institution to gather requirements, clarify dependencies, and align timelines

- Led product scoping and owned the Kick-off process during the PM’s absence to ensure the initiative stayed on track

Outcome:

Product People set the foundation for execution, enabling the bank to manage deposits efficiently, reduce risk exposure, and avoid delays in other strategic initiatives tied to liquidity management.

Initiative 3 - Boosting Repayment Plan Adoption for Overdraft Users

Problem:

Only 0.7% of eligible users were adopting repayment plans, despite them being more sustainable way to settle overdrafts.

This low adoption not only limited the bank’s ability to recover overdrafts effectively but also left many risk-prone customers paying recurring interest, rather than moving to a manageable monthly installment plan.

What has been done:

- Led the discovery phase by combining quantitative data analysis with qualitative user research. We dug into usage metrics, user paths, and drop-off points - and paired that with user interviews and feedback from customer support teams to understand pain points and misconceptions around the product.

- Our investigation revealed that most users were unaware that repayment plans even existed. Those who did find them often didn’t understand the benefits, or weren’t confident enough to commit - largely due to unclear language, poor timing, or lack of visibility.

- Based on those insights, we designed a set of experiments to test adoption levers, including:

- A new dedicated product screen that clearly explained how repayment plans work

- Multiple new entry points across relevant moments in the user journey

- Messaging and copy tests to frame repayment plans as a proactive, empowering choice - not a penalty

Outcome:

We delivered a ready-to-launch experimentation framework designed to increase repayment plan adoption, improve overdraft recovery, and transition more users into structured repayment products.

Initiative 4 - Automating Interest Rate Updates and Fixing Compliance Gaps

Problem:

Managing interest rate updates for savings products was a manual, error-prone process. On top of this, a compliance gap in Spain required dual interest rate display (gross and net)

across both frontend and backend, which had not yet been implemented. These issues increased operational workload and exposed the bank to regulatory risk.

What has been done:

- Automated the interest rate update flows, reducing manual interventions and risk of errors.

- Created a step-by-step operational playbook for interest rate updates, ensuring the process could run smoothly by any team.

- Led the full compliance fix for Spain, coordinating across product, engineering, and legal to implement dual rate display throughout the app.

Outcome:

The new automated system reduced errors and operational workload, while the compliance fix removed regulatory risk in Spain. Together, these changes created a scalable, reliable framework for managing interest rates across all markets.

Initiative 5 - Preparing the Rollout of Tiered Interest Rates

Problem:

The bank was preparing to launch tiered interest rates for its savings products, which was one of the biggest priorities for 2025.However, the initiative faced misaligned timelines and expectations across multiple teams, along with unclear product requirements.

What has been done:

- Scoped and prioritized the rollout plan, coordinating across product, engineering, legal, and design teams.

- Aligned timelines and expectations to ensure the initiative had a realistic and achievable roadmap.

- Led the redesign of the in-app savings screens, adapting the product experience to accommodate tiered rates.

Outcome:

By aligning stakeholders and defining a clear path forward, Product People unblocked a company-level priority and ensured the initiative was ready for successful execution in 2025.

Mission Achievements: Delivered Outcomes

💡Scoped and kicked off external partner integration, paving the way for scalable credit bureau connections across Europe

💡Redesigned and automated the account closure journey, reducing manual workload and minimizing reliance on collection agencies, reducing losses ~€244K

💡Prepared experiments to boost repayment plan adoption (from a current 0.7%), improving overdraft recovery potential

💡 Automated interest rate update flows and delivered a full compliance fix for Spain, removing regulatory risk

In the Client’s Own Words

Space Crew of this Mission

For Clients: When to Hire Us

You can hire us as an Interim/Freelance Product Manager or Product Owner

It takes, on average, three to nine months to find the right Product Manager to hire as a full-time employee. In the meantime, someone needs to fill in the void: drive cross-functional initiatives, decide what is worth building, and help the development team deliver the best outcomes.

If you're looking for a great Product Manager / Product Owner to join your team ASAP, Product People is a good plug-and-play solution to bridge the gap.

Interested in working with us?

Our Interim/Fractional Product Managers, Owners, and Leaders quickly fill gaps, scale your team, or lead key initiatives during transitions. We onboard swiftly, align teams, and deliver results.

.png)